by

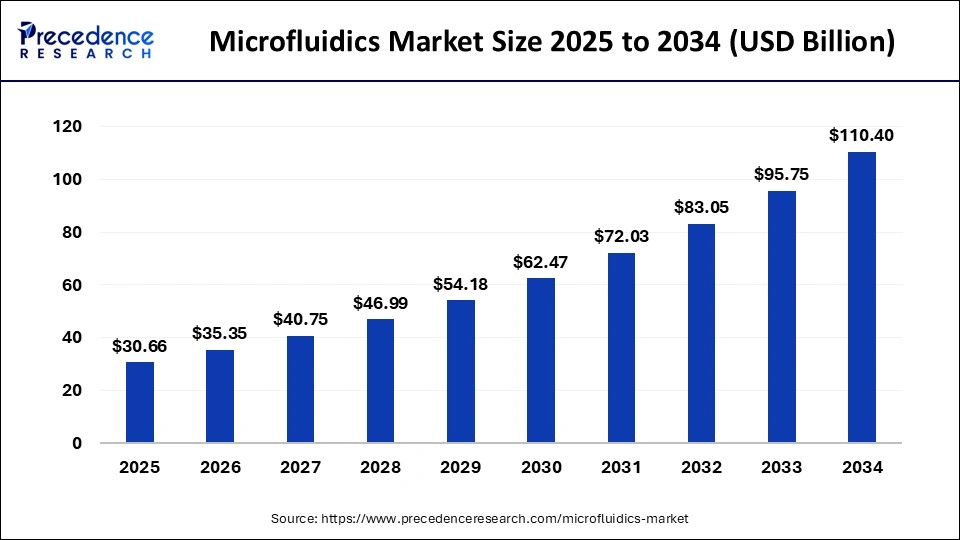

by The global microfluidics market is calculated at USD 26.59 billion in 2024 and is expected to surpass around USD 110.40 billion by 2034, at a CAGR of 15.3%.

Get Sample Copy of Report@ https://www.precedenceresearch.com/sample/1116

Key Insights

- In 2023, North America held the largest global market share at 43.13%.

- The polydimethylsiloxane (PDMS) segment led the material category with a 34.5% share.

- The medical technology segment accounted for 83% of the total revenue, making it the dominant technology.

- Among applications, the lab-on-a-chip segment stood out with the highest market share of 38%.

Market Dynamics

Market Drivers

The microfluidics market is experiencing significant growth due to the rising demand for point-of-care diagnostics and lab-on-a-chip technologies. The ability of microfluidic systems to enable rapid, accurate, and cost-effective diagnostic testing is driving their adoption across healthcare and biotechnology sectors.

Additionally, the increasing use of microfluidics in drug discovery and personalized medicine is further fueling market expansion. The miniaturization of medical devices and the integration of microfluidic technology with artificial intelligence and automation are also key factors contributing to market growth.

Market Opportunities

The expansion of microfluidics applications in areas such as wearable health monitoring devices, organ-on-a-chip models, and environmental monitoring presents lucrative opportunities for market players. Technological advancements, including 3D printing for microfluidic chip fabrication, are expected to reduce manufacturing costs and enhance product efficiency.

Moreover, government initiatives supporting research and development in life sciences and diagnostics are likely to open new avenues for industry growth. The growing adoption of microfluidics in developing regions, where affordable and portable diagnostic tools are needed, further strengthens market potential.

Market Challenges

Despite its promising growth, the microfluidics market faces challenges such as high initial costs and complexities in manufacturing. The fabrication of microfluidic devices requires specialized materials and precise engineering, which can limit accessibility for smaller companies.

Additionally, regulatory hurdles associated with medical device approvals and standardization create delays in product commercialization. Compatibility issues with existing laboratory and diagnostic equipment also pose obstacles for seamless integration into healthcare systems.

Regional Insights

North America leads the microfluidics market due to strong investments in healthcare research, high adoption of advanced diagnostic technologies, and the presence of key industry players. Europe follows closely, benefiting from government funding and an increasing focus on personalized medicine.

The Asia-Pacific region is expected to witness rapid growth, driven by rising healthcare expenditures, growing biotechnology research, and increasing awareness about early disease detection.

Microfluidics Market Companies

- Agilent Technologies, Inc.

- Illumina, Inc.

- Perkinelmer, Inc.

- Life Technologies Corporation

- Danaher

- Bio-Rad Laboratories, Inc.

- Hoffmann-La Roche Ltd

- Abbott Laboratories

- Fluidigm Corporation

- Qiagen N.V.

- Thermo Fischer Scientific

- Biomérieux

- Cellix Ltd.

- Elveflow

- Micronit Micro Technologies B.V.

Segments Covered in the Report

By Material

- Glass

- Silicon

- PDMS

- Polymers

- Others

By Technology

- Non-Medical

- Medical

- Gel Electrophoresis

- PCR & RT-PCR

- ELISA

- Microarrays

- Others

By Application

- Organs-on-chips

- Lab-on-a-chip

- Continuous Flow Microfluidics

- Acoustofluidics and Microfluidics

- Optofluidics and Microfluidics

- Electrophoresis and Microfluidics

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Ready for more? Dive into the full experience on our website@ https://www.precedenceresearch.com/