by

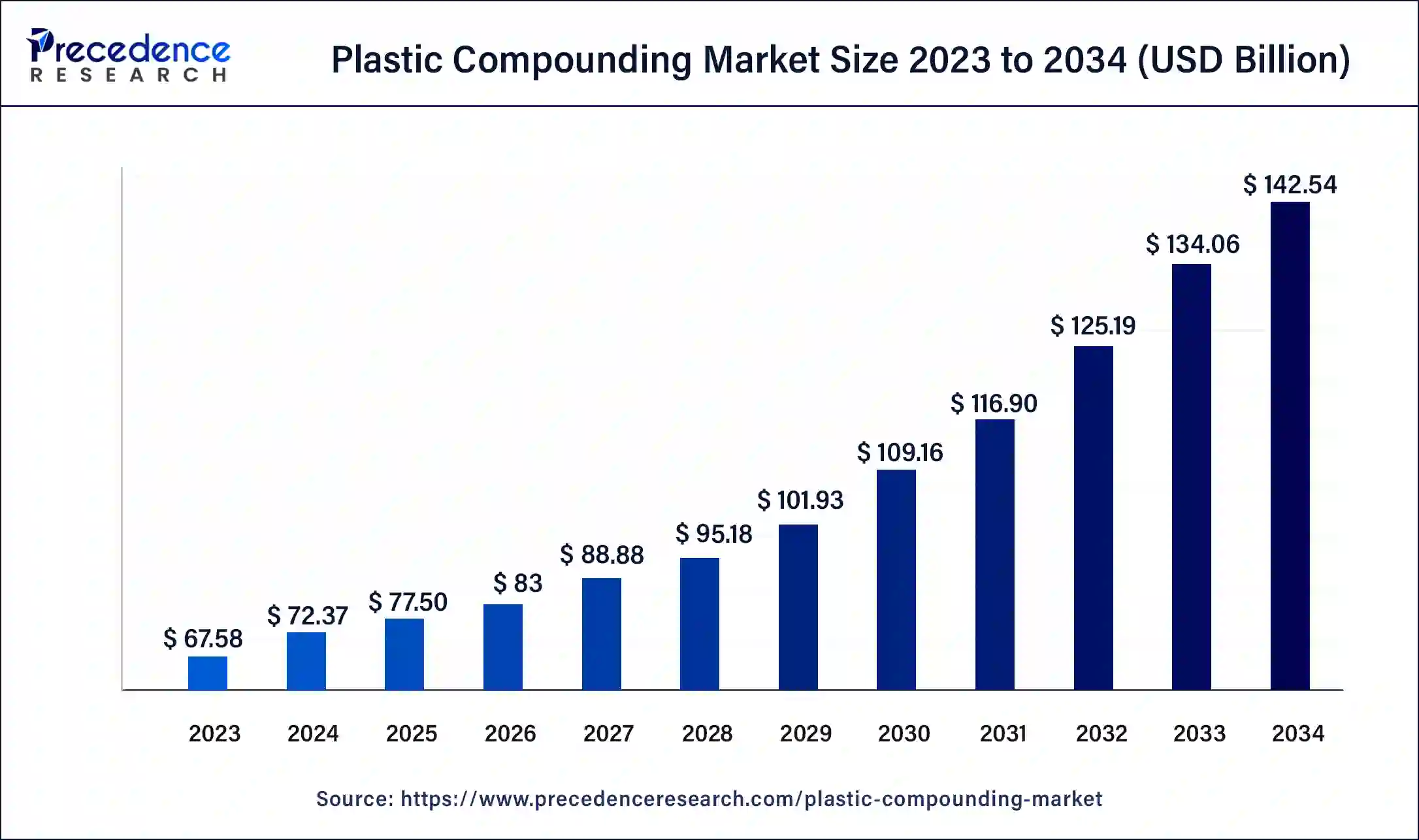

by The plastic compounding market size calculated for USD 72.37 billion in 2024 and predicted to surpass USD 142.54 billion by 2034 at a CAGR of 7%.

Get Sample Copy of Report@ https://www.precedenceresearch.com/sample/1015

Market Key Takeaway

- In 2023, Asia Pacific dominated the global market, holding the largest market share at 46%.

- The automotive segment accounted for over 26% of the total revenue share by application in 2023.

- The polypropylene (PP) segment was estimated to have the highest market share, reaching 33% in 2023.

Plastic Compounding Market Overview

The plastic compounding market is experiencing significant growth due to the increasing demand for lightweight, durable, and cost-effective materials across various industries.

Plastic compounding involves blending base polymers with additives to enhance properties such as strength, flexibility, and heat resistance. Industries such as automotive, construction, packaging, and electronics are driving demand for compounded plastics due to their versatility and performance benefits. Advancements in polymer technology and sustainability initiatives are further shaping the market’s expansion.

Market Drivers

The growth of the plastic compounding market is driven by the rising demand for high-performance plastics in automotive and construction sectors. The automotive industry is increasingly using compounded plastics to reduce vehicle weight and improve fuel efficiency.

In the construction industry, these materials are favored for their durability, corrosion resistance, and cost-effectiveness. Additionally, the growing use of plastic compounds in medical devices, consumer goods, and electrical applications is further boosting market demand.

Market Opportunities

The market presents several growth opportunities, particularly in the development of sustainable and biodegradable plastic compounds. With stricter environmental regulations and a growing focus on reducing plastic waste, manufacturers are investing in bio-based and recycled plastic compounds.

Innovations in polymer science, such as high-performance thermoplastics and advanced additive formulations, are also expanding application areas. Emerging markets, especially in Asia-Pacific and Latin America, offer significant potential for plastic compounding due to increasing industrialization and infrastructure development.

Market Challenges

Despite strong growth prospects, the plastic compounding market faces several challenges. Environmental concerns regarding plastic pollution and recycling regulations are putting pressure on manufacturers to adopt more sustainable practices.

Volatility in raw material prices, particularly for petroleum-based polymers, poses cost-related challenges. Additionally, stringent government regulations on plastic use and disposal in various regions are impacting market dynamics. Addressing these challenges requires innovation in eco-friendly materials and improved recycling technologies.

Regional Insights

Asia-Pacific leads the global plastic compounding market, driven by rapid industrialization, growing automotive production, and strong demand from the packaging and construction sectors. North America and Europe follow closely, with a strong focus on advanced materials, sustainability initiatives, and high-performance plastic applications.

Latin America and the Middle East are emerging as promising markets due to increasing infrastructure projects and expanding manufacturing industries. The global shift towards lightweight, durable, and sustainable materials will continue to drive growth in the plastic compounding market across all regions.

Market Companies

- BASF SE

- Asahi Kasei Plastics

- The Dow Chemical Company

- LyondellBasell Industries N.V.

- SABIC

- Covestro (Bayer Material Science)

Recent Developments

- In October 2022, as part of ongoing initiatives to assist clients in meeting their sustainability goals, BASF Performance Materials Asia Pacific earned several certifications at its Pasir Gudang and Pudong factories.

- In October 2022, Clariant introduces new additives at a K 2022 to aid in the sustainable development of plastics. Applications now have more resilience to facilitate prolonged use and reuse as we move toward circularity.

- In July 2022, Asahi Kasei joined European Bioplastics (EUBP), a group of businesses engaged in the production of bioplastics.

- In February 2022, Celanese Corporation and DuPont struck a legally binding agreement to purchase the majority of the latter’s mobility and material (M&M) business. Celanese is purchasing the DuPont M&M plastics portfolio, divided into two main categories: automotive and electrical/electronics.

- In February 2022, At its manufacturing facility in Paris Gudang, Malaysia, BASF SE increased the production capacity of the products Ultramid polyamide and Ultradur polybutylene terephthalate by 5,000 metric tonnes yearly.

- In January 2021, a key player named Celanese Corporation, which is a worldwide chemical and specialty materials firm, declared a rise in price in the whole plastics engineering category, citing increases in energy, transportation, and raw material prices as well as surged demand for its goods. In resultant, the company’s polyamides and PET costs are expected to climb per kg.

- In May 2019, a key player named the capacity of the plastic compounding plant based in Altamira was increased by BASF. The company further provided plastics engineering product line among which the capacity of production was increased by 15 KT per year including Ultramid and Ultradur. Therefore, this expansion surged the demand for engineering plastics in the Mexico.

Segments Covered in the Report

By Application

- Electronics & Electrical

- Automotive

- Packaging

- Building & Construction

- Industrial Machinery

- Optical Media

- Consumer Goods

- Medical Devices

- Others

By Product

- Thermoplastic Polyolefins (TPO)

- Poly Vinyl Chloride (PVC)

- Polypropylene (PP)

- Polyethylene

- Thermoplastic Vulcanizates (TPV)

- Polystyrene

- Polybutylene Terephthalate (PBT)

- Polycarbonate

- Acrylonitrile Butadiene Styrene (ABS)

- Polyethylene (PET)

- Polyamide

- PA 6

- PA 66

- PA 46

- Others

By Source

- Fossil-based

- Bio-based

- Recycled

By Regional Outlook

- North America

- U.S.

- Canada

- Europe

- U.K.

- France

- Germany

- Italy

- Asia Pacific

- China

- Japan

- India

- Latin America

- Middle East & Africa

- Saudi Arabia

- South Africa

Ready for more? Dive into the full experience on our website@https://www.precedenceresearch.com/plastic-compounding-market